It’s no secret that capital assets typically represent one of the largest values in your financial statements.

Many higher education institutions are faced with the dilemma of reduced resources and increased compliance demands in numerous administrative areas. Accurately tracking additions, retirements, and transfers not only provides financial benefits but keeps your institution compliant with federal and state requirements.

All facets of the asset lifecycle offer opportunities for process improvements that can guide your institution towards best practices. Technology continues to evolve, providing increasingly automated and cost-effective solutions in our field. While most organizations are experiencing limited resources to comply with more regulations, adopting new technology can ease your administrative burden. Finding efficiencies in current processes while addressing compliance requirements is a must to optimize capital asset practices in our institutions.

Additions / Acquisitions

Some of the most critical issues we see with asset additions are the improper capitalization of acquisitions. Each institution should have a capital asset policy in place, and property accountants or any personnel involved in the purchasing function should be trained to code these expenditures correctly.

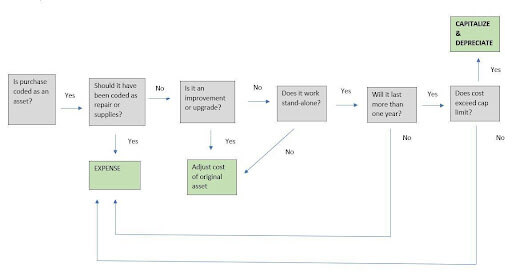

Property records must be established in an institution’s asset management system promptly upon receipt and identification of the asset. Institutions should review their purchasing process to understand how assets get added to their system, and whether acquisitions are being captured accurately. In this and other areas of asset management, communication with departments is critical to disseminate policies and procedures across your organization. Accountants who are responsible for booking asset acquisitions should have a clear decision tree to follow:

Should the purchase have been coded as a repair or supplies?

Asset-related account or expense codes should be reviewed during the acquisition process. If the purchase was coded as an asset but was a supply, maintenance, or service, it should be expensed and not capitalized regardless of the cost. Corrective journal entries should be booked in case of mistakes.

How should the purchase of an add-on or upgrade to an existing capital asset be recorded?

If a capital asset already exists in the books, any upgrades or add-ons should be added to the existing asset and depreciated. Some systems allow for adjustments directly to the existing asset, while others require a child asset to be created and connected to the parent asset. Similar issues may surface if partial payments occur during acquisition. Training of property accountants, communication with departments, and an effective tagging process are useful aids in preventing these issues.

Will the asset provide benefits for more than one reporting period?

The item should have a useful life of more than one year or one reporting period to be considered a capital asset. If the item will be consumed in less than one reporting period, it should be expensed and not capitalized, regardless of cost. Consideration of asset life should include the estimated number of years an asset is expected to be useful and functional obsolescence.

Does the purchase meet the capitalization threshold? Does each unit meet the threshold?

The capitalization threshold is the minimum cost for a purchase to be considered an asset, and it varies by institution. Purchase orders and invoices should be reviewed, and any asset that operates independently and costs over the threshold as a single unit should be capitalized. Institution-applied capitalization thresholds must be consistently applied.

Will the purchase be part of a Fabricated asset?

Fabrications are items that are built from various components to create one functional asset. Fabrication components are often miscoded as supplies and therefore expensed when they should be reviewed as possible capitalizations. If the asset will function as a system, and the aggregate costs of all the purchases will exceed the capitalization threshold, then the fabrication should be capitalized. Departments should be trained to identify fabrications and to code them accurately during acquisition.

Are moveable assets purchased under construction or renovation projects?

Be sure to review invoice documents so that moveable equipment costs are not lumped in and depreciated with the building construction. Not only will the depreciation schedule far exceed the asset’s life, but there will be untagged moveable equipment in the field, creating audit risks.