In today’s climate, there are plenty of issues that can affect property values in dramatic ways. While we can’t predict with any level of certainty what will happen next, we can prepare based on what we’re seeing today. One thing we DO know for certain, it is vital to keep up with property valuation and updating efforts.

What We Can’t Control

First, let’s look at a few things affecting property insurance today that we cannot control. These include:

- COVID-19

- CAT Loss Models

- Climate Considerations

COVID-19’s Impact on Property Values

Two simple words… demand surge. Thanks to COVID-19, we’re seeing dramatic increases in the cost to repair or replace damaged property. This trend typically occurs following a large-scale disaster when many individuals and organizations vie for a limited supply of labor and materials needed for repair.

Unlike past catastrophic events which caused regional demand surge pressures, COVID-19 is truly global in nature. Supply chains have been disrupted around the world, having domino-like effects on availability and pricing of materials.

Specific results we’re seeing:

- Steel prices are up as much as 200% since early last year.

- Lumber prices – even after coming back to earth recently – are still up 15% over pre-COVID levels.

- Copper prices are also elevated, flirting with historic highs.

- Labor costs continue to increase, especially among skilled trades.

CAT Loss Models

Every major insurer or reinsurer employs catastrophic (“CAT”) loss models to assess large portfolios of property and estimate key measures like probable maximum loss (“PML”) and average annual loss (“AAL”). At the end of the day, this predictive analysis assists the underwriters in development of their rates.

When the underlying data is inaccurate and/or incomplete, these models frequently assume worst-case scenarios, resulting in higher rates and cost of insurance. The process can be complex and involve multiple layers, dozens of specific property input variables, and several different players, including insurers, reinsurers, brokers, and even independent “scrubbers” of the data. Ever since the watershed introduction of RMS’ Version 11 (“RMS-11”), these models have accelerated in use and the corresponding level of complexity.

Climate Considerations

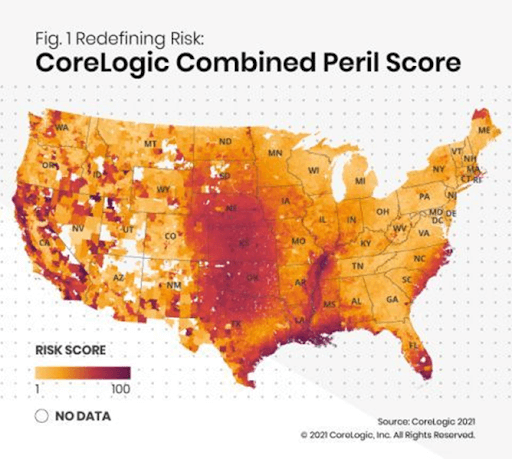

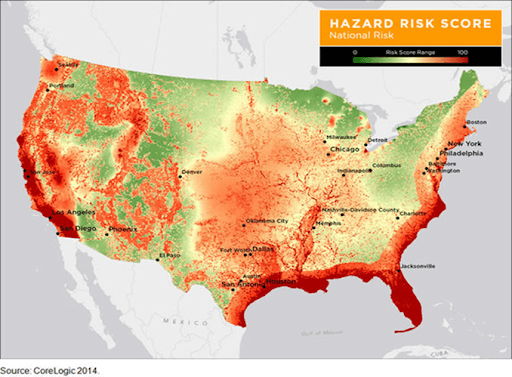

To say we’re experiencing more frequent and more severe weather events these days would be an enormous understatement. 2020 was a record year for the number of named storms in the Atlantic (30!) – a record which had stood for nearly a century. So-called “secondary” perils, such as convective storms, flooding and wildfires, are occurring at alarming rates – and on a more regular basis.

CoreLogic’s Combined Perils map below follows and scores nine risks. Comparing the 2021 map to their map from 2014 says much about the track of the last 7 years… and that trend started over 10 years ago. All these events (and their corresponding insured losses) have helped fuel the current hard market – 15 consecutive quarters, and counting.

Coverage Trends

Property remains the largest loss drag on the property and casualty (P&C) industry’s profits. Recently, the industry and property owners have faced unprecedented challenges, and insurance companies are responding with increased deductibles, reduced capacity, and changes in coverage.

What CAN You Control?

While the sky often feels like it’s falling, there are still several things that you can control (with the right help):

- Property Valuation Methodology

- Valuation Frequency & Focus

- Quality of Property Data

- Annual Adjustment of your Values

We understand the risks you’re facing. HCA regularly assists clients with detailed property inspections and appraisals, delivering accurate data your underwriters will love to see. Need help? Let’s talk today.